UK borrowing costs push above Truss-era highs

Higher central bank interest rates were among factors pushing global yields higher.

The pound has fallen markedly against the dollar, and government borrowing costs have been ratcheting up to uncomfortable highs. This inevitably spurred comparisons with Truss-era volatility and a sense of despair about UK assets – but is this fair? After all, borrowing costs – visible in bond yields – have been climbing around the world.

It’s certainly true that the UK government is in a difficult position due to a combination of self-imposed fiscal constraints and slow growth exacerbated by the Budget. But market responses to both the Kwarteng and Reeves ones should be considered in a global context.

Ten- and 30-year gilt yields have climbed significantly – but unlike in September 2022, UK borrowing costs have risen in line with those of other major economies. This is partly due to sticky inflation, and correspondingly higher expected interest rates. But it is also partly because yields on longer-dated bonds are increasing relative to those which redeem sooner, in a return to the pre-Covid norm.

As the chart below shows, in September 2022 the yield on 30-year gilts rose nearly 2 percentage points above those of the US. The situation was soon reversed, though, as Rishi Sunak became Prime Minister. Now, the spread is under half a percentage point.

UK bond yields rose alongside those of peers

Unlike the Truss-era event, longer-dated bond yields rose globally.

This leaves the government with a rather unpalatable choice. It can continue borrowing at more expensive rates while risking the wrath of the bond market. It can hike taxes further and face the backlash from voters. Or it can force more austerity.

What does this all mean for investors?

First the good news. Because money in longer-duration bonds is paid back over an extended time frame, their prices fall more than those of shorter-duration bonds. Happily, last summer we rebalanced our Global Tracker Portfolios in favour of the latter, to mitigate the risk of rising yields.

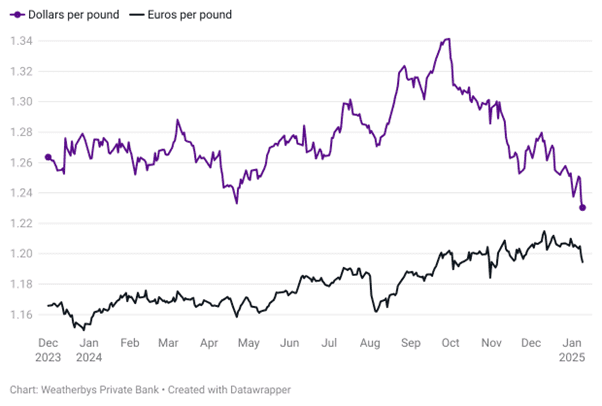

What’s more, a weakening pound benefits UK investors via their US equity holdings. Unlike many others, we do not bias portfolios towards local stocks, and so have enjoyed more of this tailwind. The charts below also illustrate that the pounds weakness relative to the dollar is a function of the latter’s strength as much as anything. The period since August has, in fact, seen the UK currency mostly trend higher against the euro.

Sterling weakened more against the dollar

Strength in US currency accounted for much of the change in exchange rate.

And finally, higher bond yields mean lower bond prices – and that could mean a more appealing investment opportunity. In short, rising gilt yields are a problem for the government, but might be an opportunity for investors. Those who thought they had missed the boat may wish to discuss the options with their private banker.

Important information

Capital at risk. Investments can go up and down in value and you may not get back the full amount originally invested.

Past Performance. Past performance is not a guide to future performance.